This post was originally published on this site.

When the world’s most vocal Bitcoin maximalist names a stock alongside BTC as a “best performing asset of the decade,” you pay attention. Michael Saylor doesn’t do diversification. He does conviction. His two bets for the next ten years are Bitcoin and Nvidia (NASDAQ:NVDA). That pairing reveals how he sees digital transformation playing out.

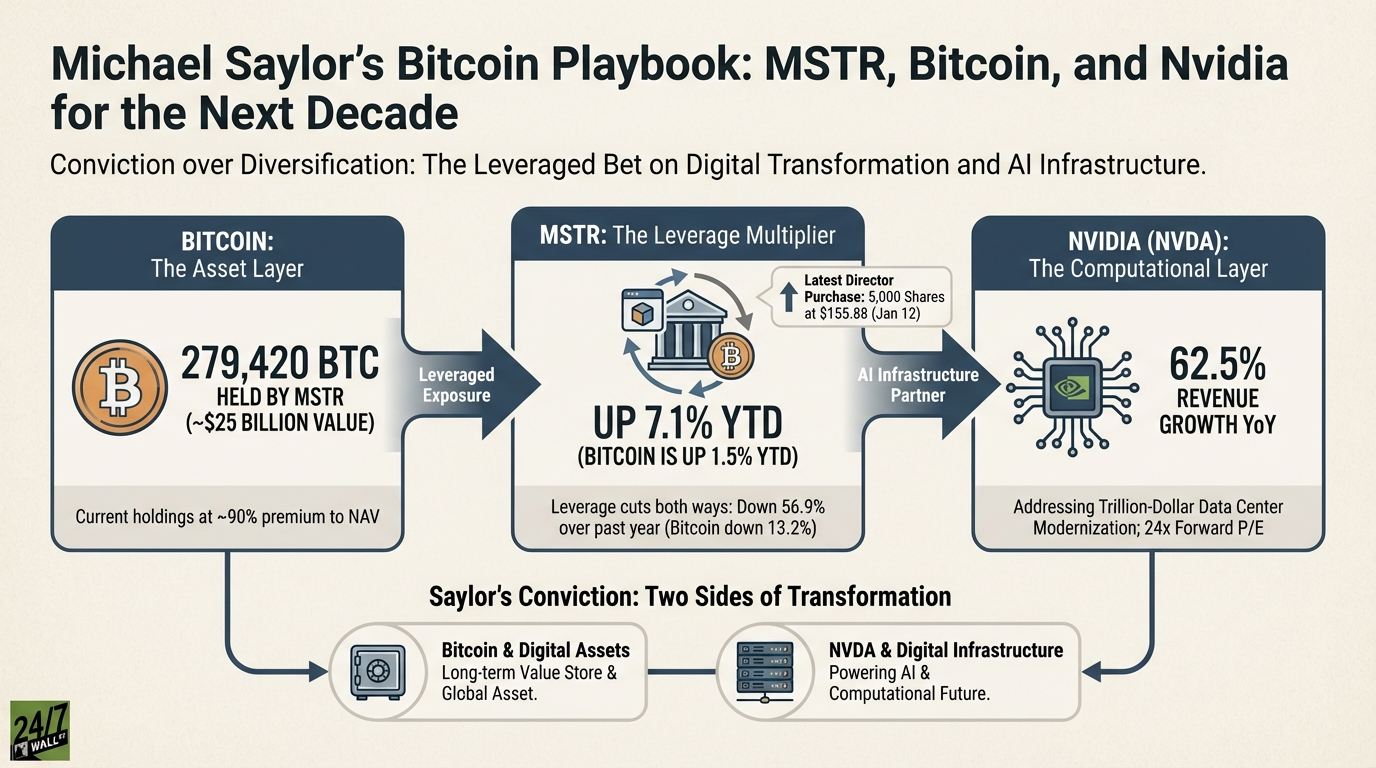

A MicroStrategy (NASDAQ:MSTR) director just bought 5,000 shares at $155.88 on January 12. That’s the first director-level open-market purchase in months, coming after executives sold heavily at $200 to $250 throughout November. When insiders stop selling and start buying after a 24% drawdown, something changed.

Saylor transformed MicroStrategy from a struggling enterprise software company into a Bitcoin Treasury Company. The playbook: issue stock and debt, buy Bitcoin, repeat. MSTR now holds $73.2 billion in Bitcoin against $8.2 billion in long-term debt. That’s not a hedge. That’s a leveraged bet.

The pairing of NVDA with Bitcoin isn’t random. Saylor sees digital assets and digital infrastructure as two sides of the same transformation. Bitcoin is the asset layer. NVDA builds the computational layer powering AI, which Saylor believes will drive the next decade of value creation.

5. The Leverage Multiplier: Understanding MSTR’s Bitcoin Bet

Bitcoin is up 1.5% year-to-date. MSTR is up 7.1%. That’s the leverage multiplier in action. When Bitcoin moves, MSTR amplifies it. The problem? It works both ways. Over the past year, Bitcoin dropped 13.2%. MSTR crashed 56.9%.

The stock trades at 7x trailing earnings, but that P/E ratio is meaningless. You’re not buying MSTR for its $128.7 million in quarterly software revenue. You’re buying it for 279,420 Bitcoin. At current prices, those holdings are worth roughly $25 billion. The market cap is $47.4 billion. You’re paying a 90% premium to net asset value for Saylor’s capital allocation strategy.

The bull case: if Bitcoin goes to $150,000, MSTR goes higher faster. The company can issue more stock at inflated prices, buy more Bitcoin, and repeat the cycle. Institutional investors who can’t hold Bitcoin directly get exposure through MSTR in their equity accounts.

The bear case? That leverage cuts both ways. MSTR carries $8.2 billion in debt. If Bitcoin enters a prolonged bear market, the premium to NAV collapses. Shareholders get diluted through more stock issuances to service debt or buy more Bitcoin at lower prices. The underlying software business? Revenue grew just 10.9% year-over-year while earnings dropped 77.5%.

Director Carl Rickertsen’s January 12 purchase at $155.88 came after the stock fell from $377 a year ago. He’s buying conviction at a 57% discount to the 52-week high.

4. NVDA: The AI Infrastructure Play Saylor Pairs With Bitcoin

Nvidia generated $57 billion in revenue last quarter, up 62.5% year-over-year. Net income hit $31.9 billion. The company prints money at a 53% profit margin while maintaining 63% operating margins. Return on equity sits at 107%.

Saylor pairs NVDA with Bitcoin because he sees AI infrastructure as the physical layer enabling digital transformation. CEO Jensen Huang laid out the addressable market on the last earnings call: “I believe that there will be no digestion until we modernize a trillion dollars with the data centers. And let’s say by 2030, the world’s data centers for computing is a couple of trillion dollars.” NVDA is capturing 80% to 85% gross margins on the infrastructure powering this shift.

The stock trades at 45x trailing earnings but just 24x forward earnings. That compression tells you the market expects growth to continue. Analysts overwhelmingly agree. Sixty of 64 analysts rate it a buy, with a consensus target of $253.19 implying 37% upside.

The tension: NVDA insiders are selling, not holding with Saylor-level conviction. CFO Colette Kress sold 200,000+ shares between November and January at prices ranging from $175 to $210. CEO Jensen Huang disposed of 9.9 million shares across 30+ transactions from October through December. These are systematic diversification moves, not panic selling. But they’re also not conviction holding.

Can NVDA sustain this valuation? If Huang’s trillion-dollar data center modernization thesis plays out over the next five years, yes. If AI investment slows or competition emerges, that 45x P/E becomes expensive fast. Saylor’s timeframe is a decade. Can you hold through a 30% to 40% drawdown if we hit a cyclical slowdown?

The Verdict: Concentration Risk With Conviction

Saylor’s playbook isn’t diversification. It’s concentration with leverage. MSTR gives you amplified Bitcoin exposure with corporate structure risk. NVDA gives you AI infrastructure dominance with valuation risk. Both require believing the digital transformation thesis plays out over years, not quarters.

The MicroStrategy director buying at $155.88 after months of executive selling suggests someone with inside knowledge thinks the Bitcoin strategy works from these levels. But remember: MSTR’s beta is 3.43. NVDA’s is 2.31. These stocks move violently. If you can’t handle watching your position drop 40% and hold anyway, Saylor’s playbook isn’t for you. But if you believe Bitcoin and AI infrastructure compound for a decade, these are the only two bets he’s making.