This post was originally published on this site.

Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE.

-

Chevron (NYSE:CVX) has signed a memorandum of understanding with Syrian Petroleum Co. and Qatar’s UCC to explore offshore oil and gas opportunities in Syria.

-

The company has also agreed to help finance Equatorial Guinea’s expanded stake in the Aseng Gas Project, deepening its role in the country’s gas sector.

-

These moves extend Chevron’s international gas and LNG reach into emerging energy markets that were not covered in earlier updates.

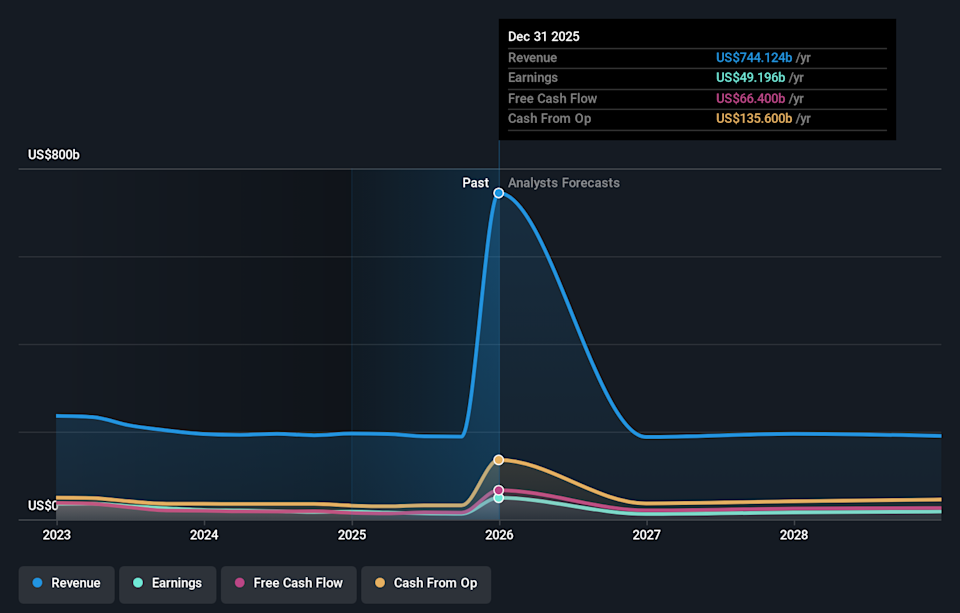

For investors watching Chevron at a current share price of $181.23, these new agreements arrive alongside solid recent stock momentum. NYSE:CVX is up 6.6% over the past week, 10.6% over the past 30 days, and 16.2% year to date, with a 24.0% return over the past year and a 142.3% return over five years.

These fresh international commitments add new geographic and project risk, but also broaden Chevron’s exposure to gas and LNG supply sources. As these agreements progress from initial memoranda and financing arrangements into on-the-ground activity, investors will be able to judge how they reshape Chevron’s portfolio mix and long-term project pipeline.

Stay updated on the most important news stories for Chevron by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Chevron.

How Chevron stacks up against its biggest competitors

These Syria and Equatorial Guinea moves plug directly into Chevron’s push to grow its gas and LNG footprint, giving it more future optionality on volumes outside its core North American shale and Guyana assets. For you as a shareholder, they sit alongside record 2025 production, ongoing Venezuela activity and the Hess integration as part of a broader effort to secure long-lived resources that can support cash generation over time, in a sector where peers like ExxonMobil and Shell are also leaning into gas-linked growth.

The new partnerships line up with the existing narrative that Chevron is leaning on large, long-duration upstream projects and international gas positions to support earnings resilience and dividend capacity through cycles. They also sit alongside management’s continued focus on cost discipline, share buybacks and a 39-year dividend growth streak. This is relevant if you are tracking Chevron as a long-term income and total-return compounder rather than a short-term trading name.

-

⚠️ Higher exposure to Syria and Equatorial Guinea adds geopolitical, regulatory and execution risk on top of the usual project timing and cost uncertainties for deepwater and gas infrastructure.

-

⚠️ Analysts have flagged dividend coverage and insider selling as watchpoints, which could matter more if large projects underperform or if commodity prices soften for a prolonged period.

-

🎁 Expanded gas access tied to facilities like Equatorial Guinea’s Punta Europa complex could support long-run LNG flows, which many investors view as an important counterpart to oil-focused volumes from Venezuela, Kazakhstan and the Permian.

-

🎁 If these projects are delivered on budget and on schedule, they could strengthen Chevron’s competitive position against global majors such as ExxonMobil and BP in supplying gas into tight regional markets.

From here, the key things to watch are how quickly the Syrian memorandum of understanding turns into concrete exploration spending, how financing for GEPetrol’s larger Aseng stake is structured, and whether Chevron continues balancing these long-cycle bets with shareholder returns through dividends and buybacks. If you want to see how other investors are thinking about these moves, take a look at the community narratives for Chevron on this dedicated page.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include CVX.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com